Economic Overview

There was one major theme from Q1, being the Russian invasion of Ukraine. While the human implications are the foremost concern, the outbreak of war offered a sharp reminder of how interconnected the world is today, and how quickly the implications of a military conflict feed back into financial markets. Commodity prices spiked as Russia is a major producer of oil, gas, and wheat, while Ukraine is also a large exporter of wheat, corn and one of the world’s largest exporters of seed oils. This, combined with ongoing supply chain issues, contributed further to the surge in inflation, while renewed Covid-19 outbreaks in China hampered their recovery. As data from Q4 was released, it showed one of the strongest years for growth across the world since the 1980’s, but more pressing issues quickly pushed any euphoria aside, resulting in Q1 being a poor one for many sharemarkets.

In the US, the Russian invasion of Ukraine was widely condemned and prompted a significant range of sanctions from the US and its allies. With the Russian economy heavily reliant on oil, President Biden banned Russian oil imports. Russian central bank assets were also frozen, as the US and its allies coordinated to deny Russia access to the global financial system.

The Russian invasion amplified inflation concerns, particularly in food and energy. In March US petrol prices recorded the biggest month-on-month increase since the oil price shocks in the mid-1970s. Other US economic data remained encouraging, with the Manufacturing and Services Purchasing Managers’ Indexes (PMI) both strong. US unemployment dropped from 3.8% in February to 3.6% in March, and while wages continue to rise, they are being outpaced by headline inflation. Annual US inflation, as measured by the consumer price index (CPI), hit 7.9% in February, which is a 40-year high. The Federal Reserve finally raised interest rates by 0.25% in March, with internal calls for further aggressive tightening and discussion of 0.5% increases.

Source: RBA 2022

Unfortunately, US consumer confidence continues to decline and according to the University of Michigan Consumer Sentiment survey, consumer confidence is at the lowest level since August 2011. Inflation is the primary culprit for the pessimism, with more consumers highlighting reduced living standards due to rising inflation. An NBC News poll saw 65% of respondents saying their family’s income is falling behind the cost of living.

In the Eurozone, the Russian invasion led to a spike in energy prices and caused much concern about ongoing energy supply. Germany suspended the approval of the Nord Stream 2 gas pipeline from Russia, while European Commission announced a plan to diversify sources of gas and speed up the roll-out of renewable energy. Either way, becoming overly reliant on Russia was a self-inflicted problem, particularly for Germany and long term plans don’t alleviate current issues, with genuine concerns high energy prices will dampen business and consumer demand. In response to rising inflation, the European Central Bank outlined plans to end bond purchases by the end of September, while ECB President Christine Lagarde suggested an interest rate rise was potentially on the cards. Data showed annual eurozone inflation at 7.5% in March, up from 5.9% in February. The flash eurozone composite purchasing managers’ index (PMI) slipped to 54.5 in March from 55.5 in February, however above 50 still represents expansion.

In the UK, The Bank of England increased interest rates by 0.5%, with two consecutive 0.25% hikes, this was on top of December’s 0.15% increase. The Office for Budget Responsibility expects UK CPI to hit 8.7% in Q4 2022 (previous forecasts had been to peak at 4.4% in the second quarter of 2022) before falling back in Q1 2023. While the UK is less exposed to energy imports from Russia than Europe, the wider impact on commodity prices only added to existing supply problems and the higher cost of energy. Chancellor of the Exchequer, Rishi Sunak, unveiled a £6 billion fiscal package to help combat the rising cost of living. UK economic data remained positive upbeat throughout the quarter, with both the Services and Manufacturing PMI showing healthy expansion. Wages continued to rise, as unemployment continued to fall.

Despite Japan’s proximity to Russia, the countries aren’t large trading partners. For Japan, Russia accounts for around 1% of exports and 2% of imports. The majority of imports are energy, specifically LNG, while exports are mostly auto-related, prompting auto makers to suspend links. The yen weakened against all major currencies in March and hit a six-year low against the US dollar as US interest rates increased. In the last week of March, the Bank of Japan conducted bond purchase operations for several days, this was a major signal the BOJ will attempt to keep bond yields near its current target rate of zero. Long-term supply constraints continued to impact growth in the automotive production industry.

In China, the number of Covid-19 cases (with Hong Kong) spiked to their highest level in two years. China’s financial capital of Shanghai, with a population of 25 million people, went into a partial lockdown at the end of the quarter in a bid to curb a surge in Omicron Covid-19 cases. Several other major cities saw lockdowns which led to the shutdown of multiple manufacturing factories, further disrupting the global supply chain. Issues such as the technology regulatory crackdown and the Evergrande debt default continued to linger, but these issues were mostly overshadowed by both geopolitical matters and and the re-emergence of Covid-19. Sentiment improved towards the end of the period as the National People’s Congress confirmed a 5.5% GDP growth target for the year.

The major Emerging market story was obviously Russia. Economic sanctions, including the removal of Russian banks from the SWIFT international payment system, led the Central Bank of Russia to increase interest rates to 20% to stem cash withdrawals by the public. Some of the world’s largest companies shuttered stores and committed to stop trade in Russia. The government also attempted to rescue the rouble, which had essentially collapsed. In response, the Central bank announced that all European payments for energy must be paid in the local currency, rather than euros or dollars. The emerging market beneficiaries were those with net commodity exports, such as Middle Eastern and Latin American countries.

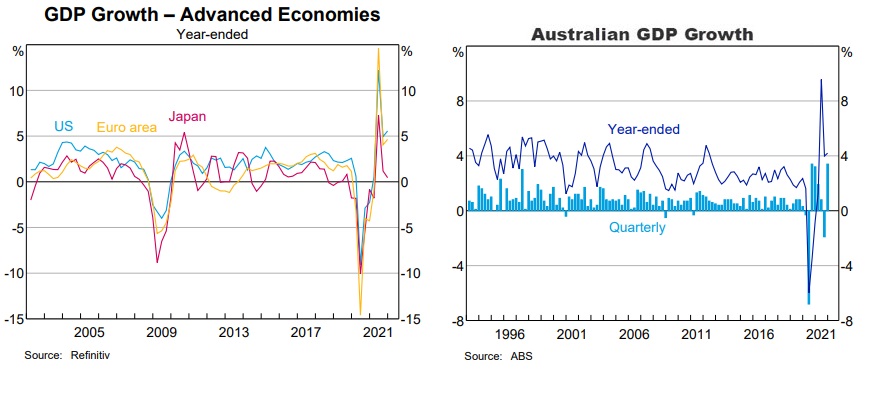

Back in Australia, data released in March 22 showed GDP increasing by 3.4% for Q4 2021, with year-on-year growth at 4.2%. This was the strongest quarter of growth since the 1970’s Household spending was up 6.3% as Australia’s two largest states moved out of lockdown in the final quarter of 2021. Not surprisingly, the big jumps came with a 24.3% increase in spending on hotels and eating out and 17.1% increase in recreation spending, as people left the house again. Unemployment data for February 22 showed unemployment at 4.0%, the lowest in 13 years. While many other central banks were raising interest rates, the Reserve Bank seemed steadfast in its language from the March meeting, noting “the Board will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range. While inflation has picked up, it is too early to conclude that it is sustainably within the target range.”

Market Overview

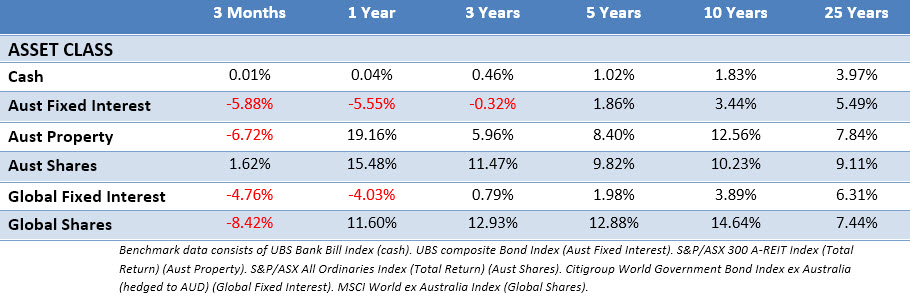

Asset Class Returns

The following outlines the returns across the various asset classes to 31st March 2022.

Global sharemarkets were volatile and quite poor in Q1. Bonds were a bigger story, with yields moving upward sharply during the quarter as the US Federal Reserve became more hawkish and pulled the trigger on a .25% rate rise. The 10-Year US Treasury yield moved from 1.51% to 2.35% with 2-year yields rising from 0.73% to 2.33%. In the UK, the 10-year yield jumped from 0.97% to 1.61%. The Australian 10-year yield moved from 1.67% to from 2.84%. All these upward movements in yields helped contribute a to fall in bond prices both globally and locally.

US shares were negative in Q1, with January and February pushing the market into correction territory, before a recovery rally for much of March. Looking at fundamentals, company earnings rebounded strongly in 2021, posting growth of 70% for the year. This reflected some of the most important sectors of the U.S. market, such as technology, communication services, health care, and consumer staples, saw few negative impacts from the pandemic, and even enjoyed stronger revenues. For the quarter, energy and utility companies were among the strongest performers, with technology, communication services and consumer discretionary the weakest.

Eurozone shares fell quite sharply in the quarter and among the worst global performers. The region has close economic ties with Ukraine and Russia, with a heavy reliance on Russian oil and gas. Energy was the only sector to see a positive return, with the heaviest falls coming in consumer discretionary and information technology sectors. Worries over consumer spending led to declines for stocks such as retailers. Austria, Ireland, Sweden, Finland, and Hungary, all saw double digit declines, while the larger French and German markets recorded mid single digit losses.

UK shares were more resilient than most of their global counterparts. The large cap FTSE 100 saw a 1.8% gain for Q1, but smaller areas of the market suffered. UK shares were driven higher by energy, mining, healthcare, and banking sectors. The UK market has a small allocation to technology, so it was far less affected than other markets. Strength in the banks reflected rising interest rate expectations, but consumer focused areas underperformed, and UK small and mid-cap shares were sold off heavily.

Japanese shares were weak in January and February, but rallied in March to end Q1 only slightly lower for the quarter. One of the bigger themes in Japanese shares was US interest rate expectations. The Fed Reserve minutes, and the 0.25% rate increase in the US, changed the market’s focus, with value-style companies outperforming growth. Much of the gain in value companies came from financial-related sectors such as banks and insurance

Asia (ex-Japan) and Emerging markets shares experienced sharp declines in Q1 amid a challenging market environment dominated by the Russian invasion of Ukraine. Share prices in China were sharply lower, while shares in Hong Kong, South Korea and Taiwan also fell. There were small pockets of growth such as Indonesia, which saw solid gains, while Thailand, Malaysia and the Philippines also moved upward.

As a whole, sentiment toward emerging markets was very sour due to Russia’s invasion of Ukraine. Despite a vast difference between various emerging market indexes, investors basically shunned the asset class, as it saw large outflows during late February and March. Russia itself was was removed from the MSCI Emerging Markets Index in early March, priced at effectively zero. Individually, commodity exporters such as Kuwait, Qatar, the UAE, Saudi Arabia, and South Africa saw good gains.

The Australian market (All Ords Accumulation) saw a 1.62% return, being one of the few developed markets to gain over Q1. The sector strength across the quarter came from energy (25%), materials (12%) and utilities (12%). Financials were incredibly volatile across the quarter with a 10% dip in January, a sharp recovery in February, before another almost 10% dip in early March, before recovering to finish up 3.6% for the quarter.

Some of the former market darlings in the buy now/pay later space were again smashed. Zip lost 65% for the quarter, despite launching a takeover for competitor Sezzle, in an attempt to consolidate the sector. It appears Afterpay accepting a takeover by US company Block was Afterpay’s founders and shareholders having the good sense to leave the party early. The sector long had its critics, and it seems the spectre of bad debts and interest rate rises are beginning to bite. In contrast, the ASX small ordinaries had a new hot sector in town, as some lithium explorers boomed across Q1.

This material is provided for information only. No account has been taken of the objectives, financial situation or needs of any particular person or entity. Accordingly, to the extent that this material may constitute general financial product advice, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. This is not an offer or recommendation to buy or sell securities or other financial products, nor a solicitation for deposits or other business, whether directly or indirectly.