Economic Overview

The major themes from Q3, namely labour and supply shortages, shipping bottlenecks and inflation, all flowed into Q4, but they were joined by a new contender for investor attention: the Omicron Covid variant. Despite Omicron being more contagious, some countries resolved to push on through the wave of infections, while others reintroduced restrictions to try and reduce the spread. As data from Q3 filtered out during Q4, it showed economic growth was slowing, but 2021 sees several major economies on track to record their strongest GDP growth in more than thirty years. Finally, some central banks have stepped up to combat inflation with interest rate rises coming fast in emerging markets.

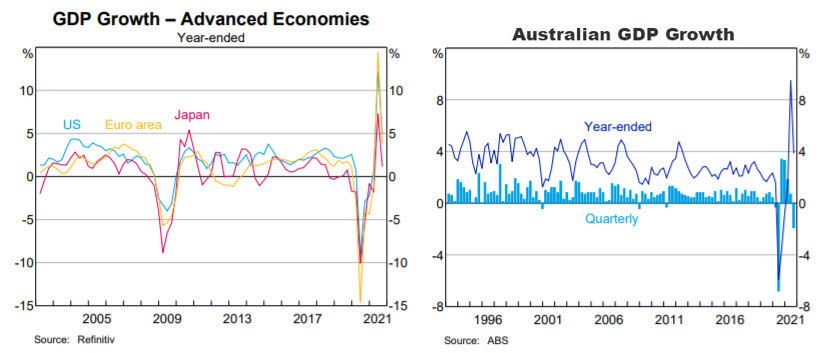

In the US, data showed economic growth slowed in the third quarter as Hurricane Ida, supply chain delays, labour shortages and Covid infections all played a role. GDP increased at 2.3%, up from an estimated 2.1%. This was the slowest quarter of growth since the historic contraction in the second quarter of 2020, as the US attempted to contain the first wave of Covid. However, economic activity was showing signs of strengthening again before a late Q4 Omicron dip. Regardless, estimates show the US economy remains on track to record its best performance since 1984, with fourth-quarter growth suggested at an annualised rate of around 7%.

Unemployment fell to 4.2% in November, the lowest figure since February 2020, down from 4.6% in October. The participation rate rose slightly, but was still about 1.5% lower than the pre-pandemic level. Inflation became a bigger topic during the quarter as annual inflation jumped to 6.2% in October and then 6.8% in November.

Source: RBA 2021

During the quarter the Federal Reserve admitted inflation has been both higher and more persistent than anticipated, with inflation significantly surpassing the Federal Reserve Open Market Committee’s 2% target. Chairman Jerome Powell also said it was time to retire the “transitory” word we’ve been accustomed to hearing, suggesting the word has different meanings to different people. While we may have thought it meant “a sense of short-lived” the Fed meaning is “it won’t leave a permanent mark of higher inflation”. If that’s not clear, we can at least be grateful we’re unlikely to hear the term “transitory inflation” again!

In the Eurozone, the Omicron variant was the dominant version in many European countries by the end of Q4. Germany, Portugal, and the Netherlands were among several countries to reintroduce restrictions on sectors such as travel and hospitality, as they tried to reduce the spread of the Omicron variant. This was on the back of a warning from the World Health Organization that a surge in cases across Europe would push health systems towards the brink of collapse. As a result, the flash PMI hit a nine-month low of 53.4 for December, as the Euro service sector was hit by rising Covid cases. Meanwhile, fuel prices were volatile and contributed to higher inflation with the Eurozone’s annual inflation rate hitting 4.9% in November, compared to -0.3% a year earlier. The European Central Bank said it would begin to scale back bond purchases, but ruled out increasing interest rates in 2022

In the UK, a big story was the surprise move from the Bank of England (BOE) to raise interest rates by 15 basis points to 0.25% in December. The rate had been at 0.10% since March 2020. The move was a surprise firstly because of Omicron, but also because despite voicing concerns in Q3 that inflationary pressures were surpassing expectations, likely to peak above 4% and remain high in 2022, the BOE underlined that it wouldn’t act in the short term. CPI inflation hit 4.2% in October and 5.1% in November, which may have helped cement the decision. The bank noted, “there was some value in waiting for further information on the degree to which Omicron was likely to escape the protection of current vaccines and on the initial economic effects of this new wave,” but “there was, however, also a strong case for tightening monetary policy now”. Q3 GDP came in at 1.1% growth, with estimates of 2021 UK GDP growing by around 6.8%.

In Japan, a general election was held in October and there were modest expectations for the ruling Liberal Democratic Party. However, the LDP lost only 15 seats and retained a decent majority in its own right. The political focus then shifted to a substantial fiscal stimulus package. The package came with direct cash handouts to households as the government attempted to kick-start a recovery after a 0.9% decline in quarterly GDP in Q3. Like elsewhere, there was short-term uncertainty as Japan had its first case of Omicron in December, but as with the prior variants, infection rates continue to remain surprisingly low by international standards. Another surprise was the strength of the rebound in industrial production which increased 7.2% October to November, fueled by a 43% resurgence in car production.

In China, factors such as the property-market downturn, triggered by the collapse of developers, flooding and power rationing, have all been drags on economic growth. Figures for Q3 showed GDP grew 4.9% annually, down from 7.9% in Q2. While some forecasts have China’s 2021 GDP figure coming in around 8%, growth is expected to slow to less than 5% in 2022. Energy usage is expected to play a larger role in dictating Chinese GDP in 2022. Pollution controls will be enacted ahead of the Winter Olympics and Paralympics across February and March, while China’s dual-control system, which aims to reduce 2020 levels of energy consumption and GDP carbon intensity by 13.5% and 18% over the next few years. This will likely lead to further power rationing.

Emerging market countries saw currency volatility and inflation continue to spike across the quarter. EM Central Banks had differing responses to their problems. The Turkish lira was extremely volatile as the central bank lowered its rate by a total of 4% to 14%, despite inflation hitting to 21.3% annually in November. With the lira under pressure, President Erdogan announced lira holders would be compensated for currency losses. In Brazil, the central bank increased rates another 3% over the quarter to counter inflation. Interest rates also increased in Mexico, Hungary, Chile, Russia, and Poland during the quarter.

Back in Australia, data released in November showed GDP fell by 1.9% for Q3, with year-on-year growth at 3.9%. The quarterly contraction was expected, due to lockdowns in NSW and Victoria, where there were falls in household consumption and services affected by the lockdowns. Government support again played a role in cushioning household and business balance sheets, with data showing the household saving rate jumping from 11.8% to 19.8% in Q3, suggesting potential for a robust recovery at some point. Late November/early December data signaled a solid rebound was already underway, but self-imposed restrictions and close contact isolations in mid to late December appeared to put a dampener on the recovery as Omicron cases spread.

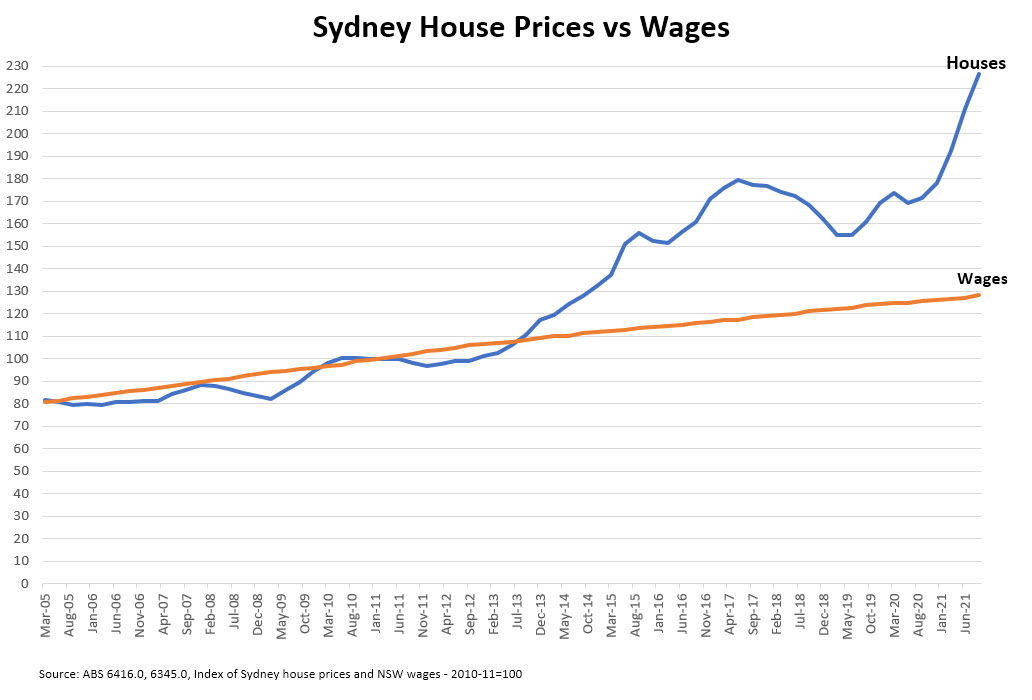

Australians continued to bid up property prices, with data from the Australian Bureau of Statistics showing the fastest rise of property prices since it first started tracking them in 2003. Combined capital city prices saw three consecutive 5%+ quarterly increases, something that hadn’t occurred in the time the ABS has kept data. Pre pandemic, Sydney house prices had attempted to move back toward wages. However, over the past year, Sydney house prices have now completely divested themselves from wages.

Data for Q3 showed 23.8% of new home loans had a debt-to-income ratio of six or higher, a threshold considered risky by the Australian Prudential Regulation Authority. A year earlier that figure stood at 16.3%. For its part, the RBA statement from December seemed unperturbed by house prices, highlighting “inflation pressures are also less than they are in many other countries” and despite market commentary around rate rises, reiterated “the Board will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range”.

Market Overview

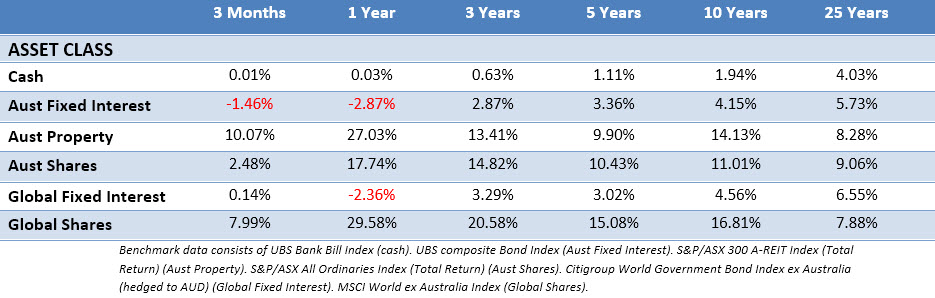

Asset Class Returns

The following outlines the returns across the various asset classes to 31st December 2021.

In Australian dollar terms global sharemarkets were very strong in Q4, overcoming some brief volatility prompted by the emergence of Omicron in the second half of the quarter. Yields rose slightly in longer dated bonds in the US. After hitting 1.7% in October and falling to 1.36% in early December, the 10-Year US Treasury yield settled at 1.51%. In the UK, the 10-year yield moved slightly downward from 1.02% to 0.97%. The Australian 10-year yield spent much of the quarter edging higher, eventually finishing at 1.67%, up from 1.48% at the end of Q3.

US shares rose in Q4. Overall gains were strong despite the weaker November, where rising Covid cases and the speed of the Federal Reserve’s asset tapering hit markets. By the end of December worries had subsided and data was indicating the economy remained stable and corporate earnings robust. This marked the third consecutive year of double-digit gains in the US with 70 new highs made by the S&P 500 during 2021. Tech was a strong performer over the quarter, with chipmakers especially strong. Real estate also shone as investors expect e-commerce to grow and drive increasing demand for industrial warehousing. Energy and financials names made gains, but were more subdued.

Eurozone shares gained over the quarter the focus turned to strong corporate profits and economic resilience, this alleviated worries about Omicron. Like in the US, markets across the Euro also drew support from data suggesting Omicron presented a lower risk of severe illness. Utilities were among the bigger winners, with IT companies notching strong gains. Technology hardware and semiconductor stocks performed particularly well while the luxury goods sector recovered from a sell off over the northern summer sparked by the “common prosperity” shift in Chinese policy. Meanwhile, the communication services and real estate sectors saw negative returns.

UK shares posted gains with the most economically sensitive areas such as banks recouping the losses seen in late November when Omicron emerged. It was a different story for sectors reliant on the economy reopening, such as travel and leisure, along with the energy sector. All were unable to make up November’s losses, posting losses for the quarter. Retailers and housebuilders gyrated with expectations of an interest rates movement, while retailers continued to struggle with supply chain disruptions. Despite the high demand, the disruptions resulted in the highest number of profit warnings in listed retailers since 2017.

Japanese shares seesawed with falls in October due to election uncertainty, but when the ruling LDP limited their election losses to a smaller number of seats than expected, a rally followed. November saw shares hit a five-month low, as news of Omicron emerged, punishing travel and tourism companies. By December, the bargain hunters emerged, and Japanese shares regained some ground as tech companies reported strong results. SoftBank was a big loser for the quarter, as its portfolio comprising large holdings in Chinese companies, such as Alibaba and Didi, ran into various Chinese regulatory hurdles.

Asia (ex-Japan) and Emerging markets were both negative in Q4, with the stronger US dollar acting as a headwind. Turkey, with its currency woes was the weakest index. China and Hong Kong were also poor performers, as there were concerns lockdown restrictions would accompany the rapid spread of Omicron. India and South Korea also ended the quarter in the red, but the declines in share prices were more modest. Chile lagged on the election of leftist Gabriel Boric as president.

Taiwan and Indonesia were strong performers, and the only two Asian markets to surpass a 5% gain for Q4. In Taiwan, a rise in exports boosted investor confidence, with chipmakers and IT companies performing well. The Philippines, Mexico and Malaysia also ended the quarter in positive territory. Peru, the UAE, and Egypt all posted double digit gains.

The Australian market (All Ords Accumulation) almost notched 2.5% return for the quarter to deliver almost 18% for the year. Q4 strength was found in real estate (REITs delivered a double-digit return), communication, utilities, and materials, which bounced after a large sell off in Q3. Most other sectors were either slightly up or slightly down for the quarter without much decisive movement either way. The real punishment for the quarter came in the buy now/pay later space. Afterpay, which was hitched to US company Block, due to a script takeover, fell over 30% during the quarter. Many of Afterpay’s smaller imitators saw similar results as the prospect of more regulation in the space loomed.

This material is provided for information only. No account has been taken of the objectives, financial situation or needs of any particular person or entity. Accordingly, to the extent that this material may constitute general financial product advice, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. This is not an offer or recommendation to buy or sell securities or other financial products, nor a solicitation for deposits or other business, whether directly or indirectly.