Economic Overview

Global policy makers expressed a cautious welcome for continuing signs of improving activity during the March quarter. The Reserve Bank of Australia noted a pick-up in global trade and industrial production, alongside a tightening of labour markets.

In the US, economic data continued to be supportive. Non-farm payrolls were robust and activity indicators buoyant. Manufacturing purchasing managers’ index (PMI) increased and the consumer confidence index rose to its highest level in 16 years.

Reflecting the improving outlook for growth and inflation the Federal Reserve increased rates by 0.25% in March. Optimism over Donald Trump’s plans to cut taxes, boost infrastructure and reduce the regulatory burden, however, the failure to pass changes to healthcare legislation raised doubts over Trump’s ability to implement some of his policies.

In the Eurozone, the period started on a weak note, with negative returns in January, but sharemarkets picked up as the quarter progressed. Economic data released during the period was largely positive. Leading indicators showed gains with the flash composite purchasing managers’ index reaching a near six- year high of 56.7 in March. Inflation, as measured by the consumer price index, picked up to 2.0% in February, albeit slipping back to 1.5% in March.

he Bank of England upgraded its 2017 UK GDP growth projection (from 1.4% to 2.0%) due to stronger-than-expected consumer spending following the “leave” decision in the EU referendum.

After weakening at the end of 2016, the Japanese yen appreciated gradually in the past three months. From Japan’s perspective, the main political event was the meeting between Prime Minister Abe and President Trump which was surprisingly cordial despite the previous US rhetoric around trade and Japan’s foreign exchange policy.

In China, better-than-expected data and a stabilizing yuan led to improved sentiment among investors. Ongoing restrictions on the property market and a tightening on capital outflows also saw liquidity diverted into equities.

Energy was a commodity laggard. Crude oil fell 6% over the quarter amid doubts over the sustainability of an OPEC-led output deal. Oil producers Norway and Russia were the worst performing developed and emerging markets respectively.

Market Overview

Asset Class Returns

The following outlines the returns across the various asset classes to the 31th March 2017.

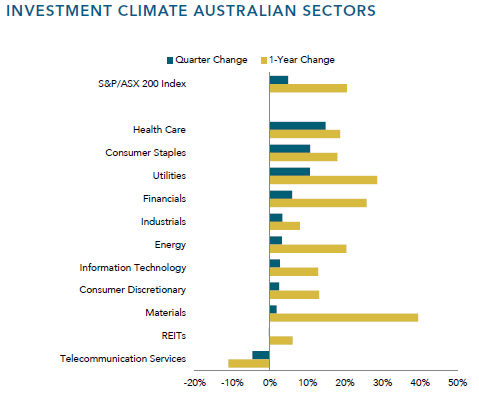

Global equity markets delivered mostly positive returns, led by emerging markets. The Australian market was a top performer, with healthcare companies being a standout with consumer staples following. However, a stronger Australian dollar trimmed gains from other developed markets for unhedged investors.

US equities performed well as the S&P 500 advanced 6.1%, Information technology was the top-performing sector, followed by consumer discretionary and healthcare.

The quarterly earnings season was a positive one for European equities, with many firms reporting double digit earnings growth and confident outlooks for 2017. The information technology sector was the top performer, followed by utilities and industrials.

The Japanese sharemarket traded in a tight range throughout the quarter, registering a total return of just 0.6%. In China, stocks gained strongly and had their best first quarter in over 10 years, driven on by continued positive news for the world’s second-largest economy.

The emerging markets posted strong gains, with US dollar weakness providing a tailwind for returns. Real Estate Investment Trusts experienced negative returns for a second consecutive quarter, although this came after several years of strong gains.

Buffett’s Bet Poised to Pay Off

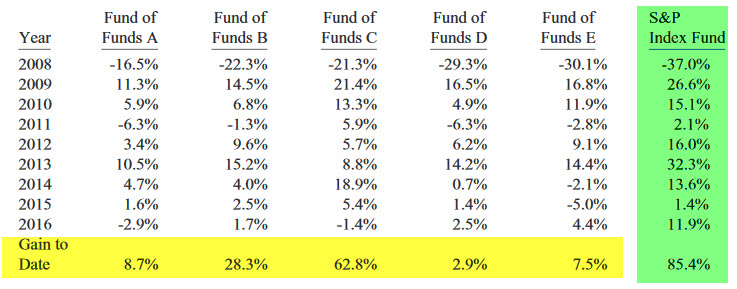

Midway through the quarter Warren Buffett released Berkshire Hathaway’s annual letter to shareholders. Most notable was Buffett highlighting his now million-dollar charitable bet with an asset manager that no investment pro could select at least five hedge funds to keep pace with an S&P 500 index fund over ten years.

Buffett publicly offered the wager back in 2006. However, in an industry where active managers base their performance on beating indices such as S&P 500, only one man, Ted Seides of Protégé Partners, stepped up to take Buffett’s challenge.

Seides picked five funds (which would not be publicly disclosed) and their performance would be averaged and then compared against Buffett’s choice of Vanguard’s S&P 500 index fund.

After nine years the results haven’t been good for the hedge funds.

The average return of the hedge funds over the past nine years was 2.2% per annum meaning $1 million invested would have gained $220,000. In contrast the inexpensive index fund Buffett chose returned 7.1% pa, which is a ballpark return for US or Australian sharemarkets over longer periods of time. The gain on $1 million invested would have been $854,000.

You’ll note, if this performance is consistent in the final year of the bet, Buffett’s investment will double in ten years, while the hedge funds will have just kept ahead of US inflation.

Buffett said of the hedge fund managers:

I’m certain that in almost all cases the managers at both levels were honest and intelligent people. But the results for their investors were dismal – really dismal. And, alas, the huge fixed fees charged by all of the funds and funds-of-funds involved – fees that were totally unwarranted by performance – were such that their managers were showered with compensation over the nine years that have passed.

And he noted why it’s hard to find a successful active manager who will be worth their fees:

Further complicating the search for the rare high-fee manager who is worth his or her pay is the fact that some investment professionals, just as some amateurs, will be lucky over short periods. If 1,000 managers make a market prediction at the beginning of a year, it’s very likely that the calls of at least one will be correct for nine consecutive years. Of course, 1,000 monkeys would be just as likely to produce a seemingly all-wise prophet. But there would remain a difference: The lucky monkey would not find people standing in line to invest with him.

We would note if it came down to a monkey or an active investment manager, there’s no guarantee of exceptional performance from either, but the monkey’s fees will be much more reasonable.

With thanks to DFA Australia.

This material is provided for information only. No account has been taken of the objectives, financial situation or needs of any particular person or entity. Accordingly, to the extent that this material may constitute general financial product advice, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. This is not an offer or recommendation to buy or sell securities or other financial products, nor a solicitation for deposits or other business, whether directly or indirectly.